CVX Stock Price Forecast 2026 to 2030; Here is analyst opinion

New York, 30 January 2026: Chevron Corporation (NYSE: CVX) is one of the world’s leading energy companies, working in oil and gas production, refining, and the new energy sector. At the beginning of 2026, the company’s stock price is around $171, and according to various analysts, future growth prospects look attractive.

This article discusses in detail Chevron’s stock price estimates, analyst predictions, the company’s pros and cons, future plans, total returns for investors, and the impact of US government energy policies on the company. This information is based on various reliable sources such as CoinCodex, Benzinga, StockScan, and others.

CVX Stock Price Forecast 2026 to 2030

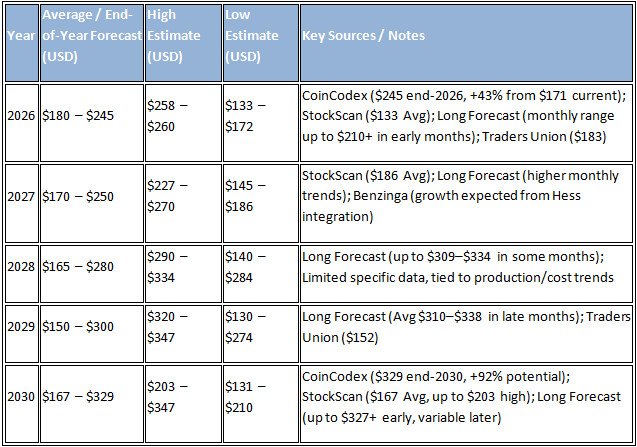

Chevron’s stock price estimates vary according to different sources, but most analysts are positive. Growth in the company’s production, acquisitions (like Hess), and investments in the low-carbon energy sector are expected to drive future growth. Here are the key estimates:

- CoinCodex’s estimate: $244.84 by 2026 (+43% from now), $328.86 by 2030 (+92%). This model is based on the company’s product growth and market position.

- StockScan.io: Average $166.93, high $203.13 and low $130.74 by 2030. This is based on financial reports and earnings history.

- Long Forecast: Starting at $152 in January 2026, rising to $172 to $210 in February. These provide monthly estimates that take market volatility into account.

- Benzinga and Traders Union: Long-term growth expected due to Hess acquisition, but a drop to $152 by 2029 is possible.

These estimates depend on oil prices, global demand, and the company’s performance. On average, analysts give a ‘buy’ rating, with an average target of $173-180.

American stock market analysts’ CVX stock price predictions from 2026 to 2030

American analysts view Chevron’s stock positively, mainly due to the Hess acquisition and increased production in the Permian Basin. Most of the 21 analysts give a “buy” recommendation:

- Benzinga: $173 expected for 2026, $200+ for 2030. Hess will boost low-cost production in Guyana.

- TipRanks: 12-month average target $179.90 (+6.42%), high $206 and low $160.

- CNN and MarketBeat: average $173.33 (+2%), ‘buy’ rating. Expected $199+ by 2030.

- Seeking Alpha: Despite high valuation, low-carbon investments can drive long-term growth.

According to analysts, if oil prices drop below $60, challenges will arise, but the company’s diversity and cash flow are strong.

Pros and cons of Chevron Corporation

Chevron is an attractive company to invest in, but there are risks due to volatility in the energy sector.

Pros

- Diversity: The company works in oil, gas, refining and new energy (like renewable fuels). This reduces the ups and downs in the energy sector.

- Attractive dividend: 4.1% dividend yield, over 30 years of annual growth. Great for passive income.

- Strong financial position: low debt ratio (7.3%), cash flow strong. $27 billion return in 2025.

- Production increase: Growth in Permian and Guyana, free cash flow will rise by $12.5 billion due to Hess acquisition.

- New energy focus: $10bn+ investment in CCS, hydrogen, and renewables.

Cons

- Volatility: Price swings in the energy sector affect shares. 5.6% TSR in 2024, but -26% in 2020.

- High valuation: 22x P/E, 60% above 5-year average. Risk due to lower oil prices.

- Policy risk: Impact due to US government policies (like Venezuela sanctions).

- Limited upside: Some analysts say growth slows if oil drops below $60.

- Environmental risk: Laws on pollution and climate change cause lawsuits and expenses.

Overall, great for long-term investors, but risky for short-term traders.

Chevron Corporation’s plan

Chevron’s 2026 plan focuses on high-return projects and sustainable growth

- Capital expenditure: $18-19 billion (organic), $1.3-1.7 billion for associates. At the lower end of the long-term guidance.

- Production growth: 3-4% annual increase by 2027. 10% growth in the Permian Basin, 30% share from the Stabroek Block in Guyana. US production will exceed 2 billion barrels/day by 2026.

- Acquisitions and expansion: Hess acquisition completed, Leviathan gas expansion (Israel). $8 billion investment in the Gulf of Mexico and Eastern Mediterranean

- Low-carbon plan: $10B+ in renewable fuels, hydrogen and CCS by 2028. 100-120k barrels/day of renewable fuels by 2030.

- Performance: $1.5 billion cost cut, increased cash flow. CEO Mike Wirth says, ‘Focusing on high-return opportunities, boosting cash flow and earnings.’

The company is balancing traditional and new energy to meet global demand.

The total return Chevron Corporation gave to investors

Chevron has given investors a strong return, mainly through dividends and share buybacks

- 2024: 5.6% TSR (Stock price + dividends).

- 3-year (2022-2024): 15.8% combined annual return (less than colleagues).

- 5-year: 148.50% total return (higher than 87.63% of the S&P 500).

- 10-year: 6.1% annual TSR (less than S&P 500’s 12%).

- Historic record: $27 billion return in 2025 ($12.8 billion dividends, $12.1 billion share buybacks). 39 years of annual dividend growth.

- YTD (2026): 12.32% (up to 171.19).

These returns are based on product growth and strong cash flow, but they are affected by fluctuations in the energy market.

US government’s energy policies and their impact on Chevron’s production or service

The American government’s energy policies directly affect Chevron, mainly due to rules and restrictions:

Trump administration:

Cancelled the license in Venezuela but promised a ‘Venezuela revival’, benefiting Chevron (20% Venezuelan oil production). CEO Wirth calls for a ‘sustainable energy policy’ balancing environment, affordable energy and national security. Trump’s ‘America First’ policy will reduce regulations and increase energy production.

Chevron Deference Reversed:

The 1984 Chevron v. NRDC decision is overturned, meaning courts will challenge federal agencies (like the EPA) interpretations. This will weaken environmental rules, benefiting Chevron (less regulatory burden). But there’s a risk due to climate change and pollution rules.

California legislation:

New rules could lead to energy shortages and high petrol prices. Chevron’s chairman Andy Walz says this will make ‘California unattractive for investment’.

Overall impact:

Biden’s strict environmental rules (like the IRA) encourage low-carbon investments, but under Trump they could be reversed. This would affect Chevron’s Venezuela and Guyana production, but lower regulations would boost output in the Permian and Gulf of Mexico.

Chevron is a strong company that will face future challenges. Investors should keep an eye on market changes and policies. (Information is up to 30 January 2026.)

Related Articles