SMCI Stock Price Forecast 2026 to 2030: Here is analysts opinion

New York, 26 January 2026: Super Micro Computer Inc. (NASDAQ: SMCI) is a leading technology company specializing in server, storage, and AI-related hardware products. In 2026, the company is in a strong position amid growing demand for AI and cloud computing but faces challenges due to accounting investigations and market volatility.

These articles focus on SMCI stock price forecasts from 2026 to 2030, predictions by American stock market analysts, the company’s gains and losses, company plans, overall returns provided to investors, and the impact of US government policies on the company’s products and services. This analysis is based on various reliable sources and data available up to 26 January 2026.

SMCI Stock Price Forecast 2026 to 2030

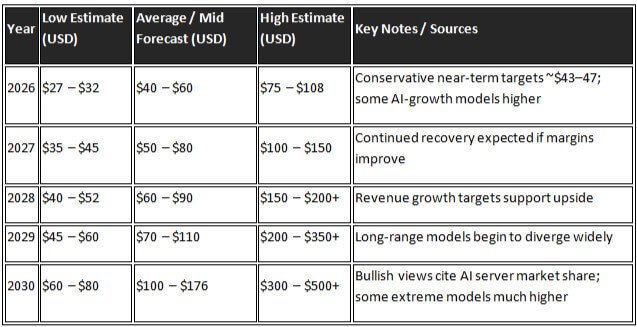

At the beginning of 2026, SMCI stock’s current price is around $31 to $45, down from last year’s highs. With the growing demand for AI infrastructure, the company’s revenue is expected to rise. According to various sources, the average price estimate for 2026 is $60.34, showing about a 100% increase from the current price. For 2027, the price could reach $76.86, $87.88 for 2028, $101.88 for 2029, and up to $127.44 by 2030. Some optimistic estimates suggest it could go as high as $176 by 2030, while others mention highs up to $482.

The table below gives an estimate of the average price by year:

These estimates are based on the growth of the AI server market, with AI-related servers expected to grow by 60% by 2030. However, market volatility and competition could change this.

US stock market analysts’ SMCI stock price predictions from 2026 to 2030

According to American analysts, SMCI stock has a ‘hold’ rating, with an average 12-month price target ranging from $43.59 to $47.43. In the long run, sources like Motley Fool expect EPS to grow at a 25% CAGR until 2030. Goldman Sachs has set a low target of $27, while Rosenblatt has a high target of $1300 (pre-split). In the latest discussions on X (formerly Twitter), chances of $100+ by 2026 are mentioned due to AI infrastructure demand. Overall, analysts are optimistic about AI growth but cautious due to accounting issues and competition.

Pros and cons of Super Micro Computer Inc.

Pros

- Strong position in AI and cloud: The company is leading in AI servers and data center hardware, with solid ties with partners like NVIDIA and AMD. This is profitable due to the growing demand for AI.

- Low valuation: Forward P/E at 12-13, the company is undervalued and has 2x+ growth potential.

- Revenue boost: $36 billion expected by 2026, thanks to AI-driven customer demand.

- New products: Innovation in liquid cooling and data center solutions.

Cons

- Accounting and regulatory issues: Stock volatility due to federal investigation and allegations of accounting fraud.

- Competition: Pressure from companies like Dell and HP, which reduces margins.

- Volatility: The stock price keeps changing, with a 50% fluctuation.

- Profit conversion issue: revenue is increasing but free cash flow is decreasing.

Super Micro Computer Inc.’s plan

The company’s plan focuses on expanding its AI infrastructure. It’s entering the government market by setting up a US federal entity, which includes a US-based product and AI server portfolio. There’s an emphasis on building a new tech campus in San Jose, increasing production capacity, and innovations like liquid cooling. They aim for $36 billion in revenue and $11 billion in quarterly sales by 2026, including global expansion and cloud penetration.

Total return given to investors by Super Micro Computer Inc.

The company has historically given strong returns. 246.24% in 2023, 86.80% in 2022, and an average annual return of 28.64% over the last 10 years. 2026 YTD is 10.86%, but in the past 12 months, it’s -4.16%. Long-term investors have benefited from AI growth, but the recent dip means the TTM average is 3.76%.

The impact of American government policies on Super Micro Computer Inc.’s products and services

The US government’s policies have mixed effects on the company. On the positive side, a new US federal entity has been launched for expansion in the federal market, which includes US-based production and AI server supply. This is beneficial for government contracts and supporting American innovation. On the negative side, accounting audits and accusations of sanctions violations have led to a drop in the stock. Trump’s tariffs and export restrictions to China have affected the supply chain, including the export ban on H20 chips, which has reduced revenue. Overall, the US-based production strategy is profitable, but trade restrictions are challenging.

This article is based on market changes and is not investment advice. Get professional advice before investing.

Related Articles